Metalico Reports Record Second Quarter Earnings

CRANFORD, NJ, Jul 31, 2008 (MARKET WIRE via COMTEX News Network) — Metalico, Inc. (AMEX: MEA) today reported the best quarter in the Company’s history, with sharp increases in revenues, operating income and EBITDA for the second quarter of 2008.

Highlights of the second quarter include:

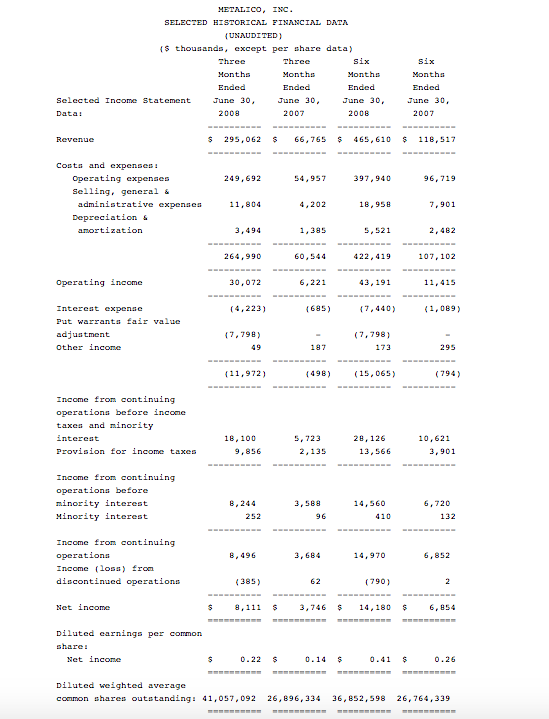

— Sales increased by 342% to $295.1 million in 2008, compared to $66.8

million in the prior year’s second quarter.

— Operating income increased by 383% to $30.1 million, compared to

operating income of $6.2 million for the quarter ended June 30, 2007.

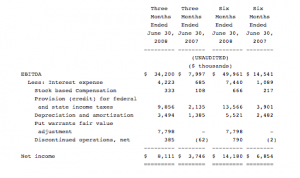

— EBITDA (as defined below) increased by 328% to $34.2 million, compared

to $8.0 million in the second quarter of 2007.

Net income for the quarter ended June 30, 2008 was $8.1 million or $0.22 per share (on a diluted basis) after the effects of SFAS No. 150 accounting treatment described below, and after a loss in discontinued operations of $.4 million or $.01 per share, compared to net income of $3.7 million or $0.14 per share (on a diluted basis) in the second quarter of 2007.

SFAS No. 150

If not for the effect of SFAS No. 150, the Company earned $15.9 million or $0.41 per share in the second quarter. Actual results include an accounting charge for a non-cash, non-tax-affected item for warrants issued in connection with equity and debt financings closed by the Company during the second quarter. The charge reduced fully diluted net income for the quarter by $7.8 million or $0.19 per share.

The warrants are classified as a liability, under SFAS No. 150, because the warrant agreement contains a cash redemption provision that is triggered only in the event of a change of control. The warrants are measured at fair value both initially and in subsequent periods. Changes in fair value of the warrants are reported as “put warrants fair value adjustment” in the Company’s consolidated statements of income. The initial valuation of the warrants was $7.1 million and as stated above the change in value from the initial valuation date through June 30, 2008 was $7.8 million.

The total put warrant liability was $14.9 million as of June 30, 2008. The liability is recorded in the Long-Term Liability account titled “put warrant liability.” Shareholders’ equity was negatively impacted by the cumulative liability required under SFAS No. 150 for warrants described above. No legal obligation exists to repurchase the warrants at this time.

Operating Results

Metalico’s Scrap Metal segment experienced quarter-over-quarter unit volume increases of approximately 185% for ferrous and 93% for non-ferrous metals. Excluding the contribution of operations acquired in the second quarter, and despite a weakening economy, Metalico achieved sequential quarter-over-quarter unit volume increases of 11% for ferrous and 4% for non-ferrous metals. The Lead Fabricating volume decreased by 23% quarter-over-quarter.

Ferrous metal prices saw an increase of 126% quarter-over-quarter. Selling prices for non-ferrous rose by 215% quarter-over-quarter, largely driven by the high unit selling price of Platinum Group Metals (“PGM’s”), which are priced in troy ounces, relative to other non-ferrous metals priced in pounds. PGM’s were the largest source of non-ferrous revenue for the Company in the quarter and for the first half of 2008.

The Lead Fabricating segment returned to an operating profit in the second quarter of 2008 as a result of improved operating margins.

Excluding corporate overhead, the Company’s Scrap Metal segment enjoyed a 605% gain in operating income in the second quarter of 2008 over the second quarter of 2007 from $4.5 million to $31.5 million. The Lead Fabricating segment achieved operating income of $1.5 million in this year’s second quarter, compared to the historical high operating income of $3.5 million in the prior-year period. Through June 30, 2008, Lead Fabricating segment sales dropped to under 10% of year-to-date revenue.

Commenting on the results for the quarter, Carlos E. Agüero, Metalico’s President and Chief Executive Officer, said, “We are extremely pleased with our performance and the favorable trends in the steel industry which derivatively carried over to scrap metals recycling. We are also pleased with the expanding contributions of recently acquired companies and the progress being made integrating this year’s acquisitions.

“We benefited from strong PGM pricing and especially from record ferrous metal prices, which continued to rise throughout the second quarter, coupled with significant unit volume growth for both metals.”

He added, “No doubt these are extraordinary times given the unprecedented pace and breadth of consolidation occurring throughout the metals industry. But the supply and demand of desirable acquisition opportunities appears to be shifting to over-supply, which should bode well for Metalico’s acquisition strategy.”

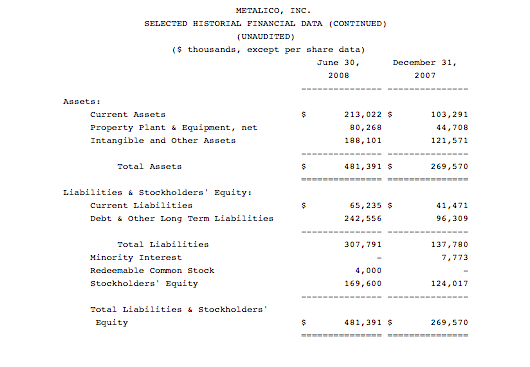

Debt and Shareholders’ Equity

Metalico’s outstanding debt increased to a total of $223.5 million as of June 30, 2008 from $121.8 million at March 31, 2008, a difference of $101.7 million, resulting largely from financing approximately $74 million for the acquisition of the assets of The Snyder Group in western Pennsylvania and West Virginia and other capital expenditures. Shareholders’ equity increased by 7.9% or $12.4 million to $169.6 million as of June 30, 2008, from $157.2 million as of March 31, 2008.

The Company’s future results will not reflect the consolidation of its investment in Beacon Energy Holdings, Inc., a biodiesel development stage company. The Company no longer holds a controlling interest in Beacon because its ownership has diminished to only 36.6% of Beacon’s outstanding stock.

As of June 30, 2008, Metalico had 36,037,292 common shares issued and outstanding. The Company has no outstanding preferred shares.

Metalico operates in the highly cyclical and volatile commodity metals universe, made even more difficult by the volatile and unpredictable economic and capital market conditions. The Company’s core business strategy emphasizes balanced growth of the ferrous, non-ferrous and PGM Metal Recycling business through acquisitions or new facility expansion and development in existing and new geographic markets.

Metalico’s stated goal is to maintain and enhance its status as a leading producer of recycled metal in the markets where it operates, focusing on broad diversification among various commodity metal groups and taking a long-term view to achieve above-average growth and financial performance.

Outlook and Update

The Company said it believes results for the third quarter of 2008 may be influenced by several factors:

— First and foremost, Metalico expects continued contributions from

companies acquired within the last twelve months.

— Ferrous scrap metal pricing has remained near record levels into the

third quarter, with international and domestic demand expected to remain

relatively strong.

— Non-ferrous prices appear to be settling in a trading range lower than

what was experienced during the first half of 2008. The Company

anticipates sluggish third quarter pricing for stainless steel and copper

and normal flow and steady prices of aluminum.

— Average PGM prices, early in the third quarter, are off of their

record levels, but appear to be settling in a narrow but lower trading

range. This may have the effect of reducing unit PGM volume growth in the

catalytic converter business, but it is unclear yet what impact lower PGM

prices could have on margins. Although competition for market share should

continue to be intense, Metalico expressed confidence in its ability to

further grow this part of the business.

— The Lead Fabricating segment has worked through high cost inventory,

returning to positive cash flow contribution which should continue into the

third quarter. Selling prices for fabricated lead products should remain

stable. The Company anticipates seasonably higher unit volumes during the

warm months tempered by the negative impact of continued economic slowdown.

Metalico’s objective is to complete at least one more transaction before the end of 2008. However, completion of any additional acquisitions in 2008 will be subject to reaching satisfactory business terms, completion of due diligence, signing definitive purchase agreements, and raising debt and equity capital on reasonably acceptable terms. There can be no assurance that Metalico will be successful in completing any of the above. Metalico continues to evaluate a large and diverse number of mid-size and large acquisition opportunities.

Metalico intends to continue acquiring successful platform operations in strategic geographic markets with the added objective of remaining independent and continuing to be an aggressive acquirer and consolidator of high quality, secondary commodity metals businesses.

Metalico, Inc. is a rapidly growing holding company with operations in two principal business segments: ferrous, non-ferrous and PGM metal recycling, and fabrication of lead-based products. The Company operates twenty recycling facilities in New York, Pennsylvania, Ohio, West Virginia, New Jersey, Texas, and Mississippi and five Lead Fabricating plants in Alabama, Illinois, Nevada, and California. Metalico’s common stock is traded on the American Stock Exchange under the symbol MEA.

The Company defines EBITDA as earnings before interest, income taxes, depreciation, amortization, other income and expense, put warrants value fair value adjustment, stock based compensation, minority interests and discontinued operations. EBITDA is considered non-GAAP financial information and a reconciliation of net income to EBITDA is included in the attached financial tables.

Forward-looking Statements

This news release, and in particular its “Outlook and Update” section, contains “forward-looking statements” made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, such as Metalico’s expectations with respect to its results of operations for the third quarter of 2008, commodity pricing, volumes, and trends. These statements may contain terms like “expect,” “anticipate,” “believe,” “appear,” “estimate” and other words that convey a similar meaning, or are statements that do not relate strictly to historical or current facts. Forward-looking statements include statements with respect to Metalico’s beliefs, plans, objectives, goals, expectations, anticipations, assumptions, estimates, intentions, and future performance, and involve known and unknown risks, uncertainties and other factors, which may be beyond Metalico’s control, and which may cause Metalico’s actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. Factors that could cause such material difference are discussed in more detail in the Company’s most recent Annual Report on Form 10-K and other filings with the Securities and Exchange Commission. All statements other than statements of historical fact are statements that could be forward-looking statements. Metalico assumes no obligation to update the information contained in this news release.

Non-GAAP Financial Information

Reconciliation of Non-GAAP EBITDA and Net Income

When the Company uses the term “EBITDA,” the Company is referring to earnings before interest, income taxes, depreciation, amortization, stock based compensation, put warrants fair value adjustment and discontinued operations. The Company presents EBITDA because it considers it an important supplemental measure of the Company’s performance and believes it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in Metalico’s industry. The Company also uses EBITDA to determine its compliance with some of the covenants under its credit facility. EBITDA is not a recognized term under generally accepted accounting principles in the United States (“GAAP”), and has limitations as an analytical tool. You should not consider it in isolation or as a substitute for net income, operating income, cash flows from operating, investing or financing activities or any other measure calculated in accordance with GAAP. Other companies in the Company’s industry may calculate EBITDA differently from how the Company does, limiting its usefulness as a comparative measure. EBITDA should not be considered as a measure of discretionary cash available to the Company to invest in the growth of its business. The following table reconciles EBITDA to net income:

Contact:

Metalico, Inc.

Carlos E. Agüero

Michael J. Drury

Email Contact

186 North Avenue East

Cranford, NJ 07016

(908) 497-9610

FAX: (908) 497-1097

www.metalico.com

Share